Nursing & Healthcare Career College for Sale in Western Canada (School No. 3434)

Market-Leading Regulated Healthcare Career College Platform

Halladay Education Group presents School No. 3434, a Western Canadian regulated healthcare career college with structural advantages: 30+ years of regulatory standing, a 690+ partner practicum ecosystem (2025), and proven execution in one of Canada’s most defensible post-secondary niches. Core programs include Practical Nursing, Health Care Assistant, Community Support Worker, and Dental Assisting.

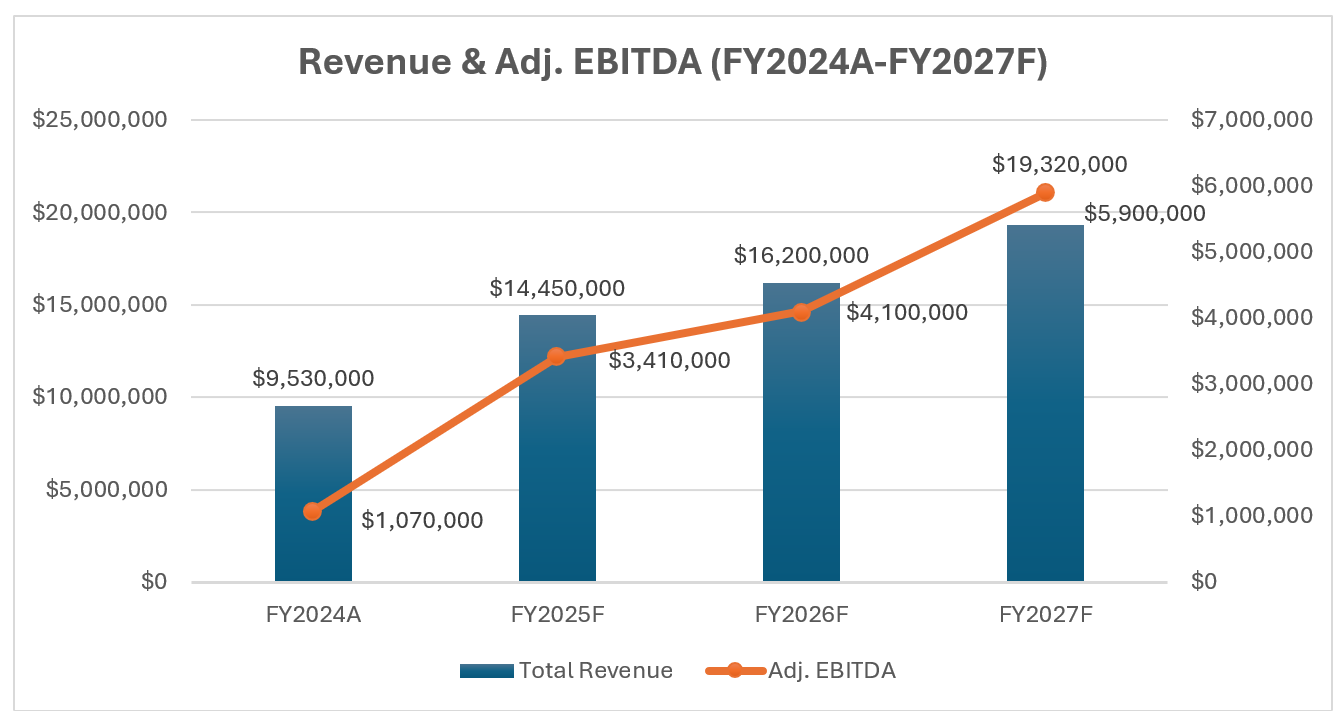

The Investment Case (FY2025 Valuation Anchor)

The platform is entering a step change in earnings, with FY2025 as the valuation reference year: $14.45M revenue and $3.41M Adjusted EBITDA (24% margin) on normalized operations within the existing footprint. Revenue grows from $8.0M (FY2023A) to $19.3M (FY2027F) (25% CAGR), driven by approved program capacity, cohort layering, and rising continuing-student density. Adjusted EBITDA expands to $5.9M, with margins reaching ~30% by FY2027F as operating leverage is realized. Growth requires no new campuses or material capex, primarily instructor hiring and optimized scheduling.

Market Position: Demand and Defensibility

The college’s program mix directly addresses persistent provincial healthcare workforce shortages. This demand is structural, not cyclical, supporting sustained enrollment across economic conditions. Management reports 690 unique practicum partners (2025) supported by a substantial clinical and preceptorship network, underpinning throughput and outcomes, including 92% program completion (2025 graduates) and 92% job placement (2024 graduates).

The Regulatory Fortress (Barriers to Entry)

Provincial designation, student-aid eligibility, federal DLI status, and program-level healthcare licensing requirements create significant barriers to entry. Maintaining approvals depends on long-standing compliance, outcomes, and audit-ready operations. Replication typically requires multiple approval cycles and multi-year relationship-building with health authorities and clinical partners. Practicum access is the binding constraint in healthcare education; this platform’s placement network supports throughput and scale within the current footprint.

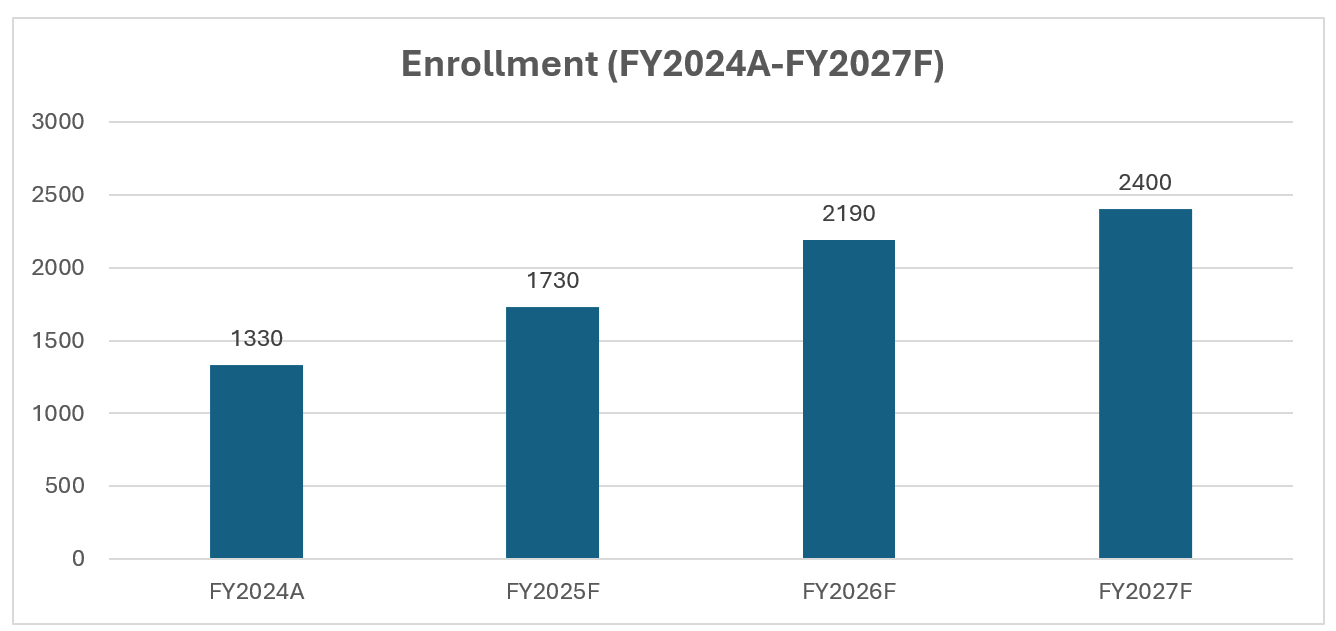

The Financial Story: Scale Without Capital

Growth is driven entirely by operational levers with no facility expansion required:

- Cohort Layering: Total enrollment grows from 1,330 (FY2024A) to 2,400 (FY2027F)

- Continuing Students: 470 → 985, improving density and revenue visibility

- Operating Leverage: Fixed costs absorbed as utilization increases

- High-Quality Earnings: Normalization addbacks decline from $370K (FY2024A) to $60K (FY2027F) (≈1% of projected EBITDA)

Revenue Quality: Tuition-Led, Not Grant-Dependent

Revenue is anchored in domestic tuition, not immigration flows or discretionary grants. Domestic tuition students accounted for 74% of enrolment (FY2024A) and increased to 99% by FY2027F, reducing exposure to immigration policy volatility and grant timing uncertainty.

- Conservative Grant Treatment: Base case includes only booked or contracted awards

- Potential Upside (if awarded): Pending grant applications are excluded from the base case

Operating Strengths

- Multi-Location Flexibility: A multi-campus footprint enables flexible cohort deployment across markets with the highest demand and practicum availability, reducing geographic concentration risk.

- Capital-Light Expansion: The growth forecast requires no new campus openings, only instructor hiring and optimized scheduling within current facilities.

- Transaction-Ready: Tenured leadership, complete regulatory documentation, audited financials, and established systems support streamlined diligence.

Investment Highlights

- Scarce Regulated Asset: 30+ year, provincially designated, multi-campus healthcare platform that is difficult to replicate

- Margin Expansion in Flight: Adjusted EBITDA margins expand from 24% (FY2025) to ~30% (FY2027F)

- Supply-Constrained Market: Growth limited by practicum capacity and approvals, not student demand

- Structural Demand: Workforce shortages drive steady enrollment

- Tuition-Led Revenue: Reduced immigration and grant dependency; pricing upside not assumed

- Multiple Expansion Paths: Add-ons, program expansion, regional densification

- De-Risked Base Case: Flat tuition and excludes pending grants, leaving upside potential

Why Now

The college is at an inflection point: enrollment momentum is building, regulatory frameworks are stable, and healthcare workforce shortages continue across Western Canada. With growth occurring within the existing footprint, a buyer can focus on execution levers such as utilization, program mix, and selective tuck-in opportunities.

Next Step

If you would like to explore this opportunity further, please click here to review the Teaser Doc and contact us to request an NDA. Upon execution, you’ll receive the Confidential Information Memorandum and access to the secure data room.

📞 Call us toll-free at +1.800.687.1492

📧 Email info@halladayeducationgroup.com